Should your credit history from ten years ago determine your loan approval today? Traditional scoring systems think so. AI disagrees.

- AI credit scoring analyzes vast traditional and alternative data to predict loan repayment more accurately than traditional models.

- Models use machine learning, continuous learning, and regular validation to improve accuracy and adapt to changing conditions.

- Benefits for lenders include reduced defaults, faster decisions, lower costs, expanded markets, and improved fraud detection.

- Benefits for borrowers include fairer evaluation, faster approvals, expanded access for thin-file applicants, and better pricing.

- Risks include algorithmic bias, explainability challenges, data privacy concerns, and the need for strong model risk management and governance.

Millions of creditworthy borrowers get denied loans every year. Their thin credit files or unconventional financial histories make them invisible to traditional scoring models. Meanwhile, lenders miss profitable lending opportunities hiding in plain sight.

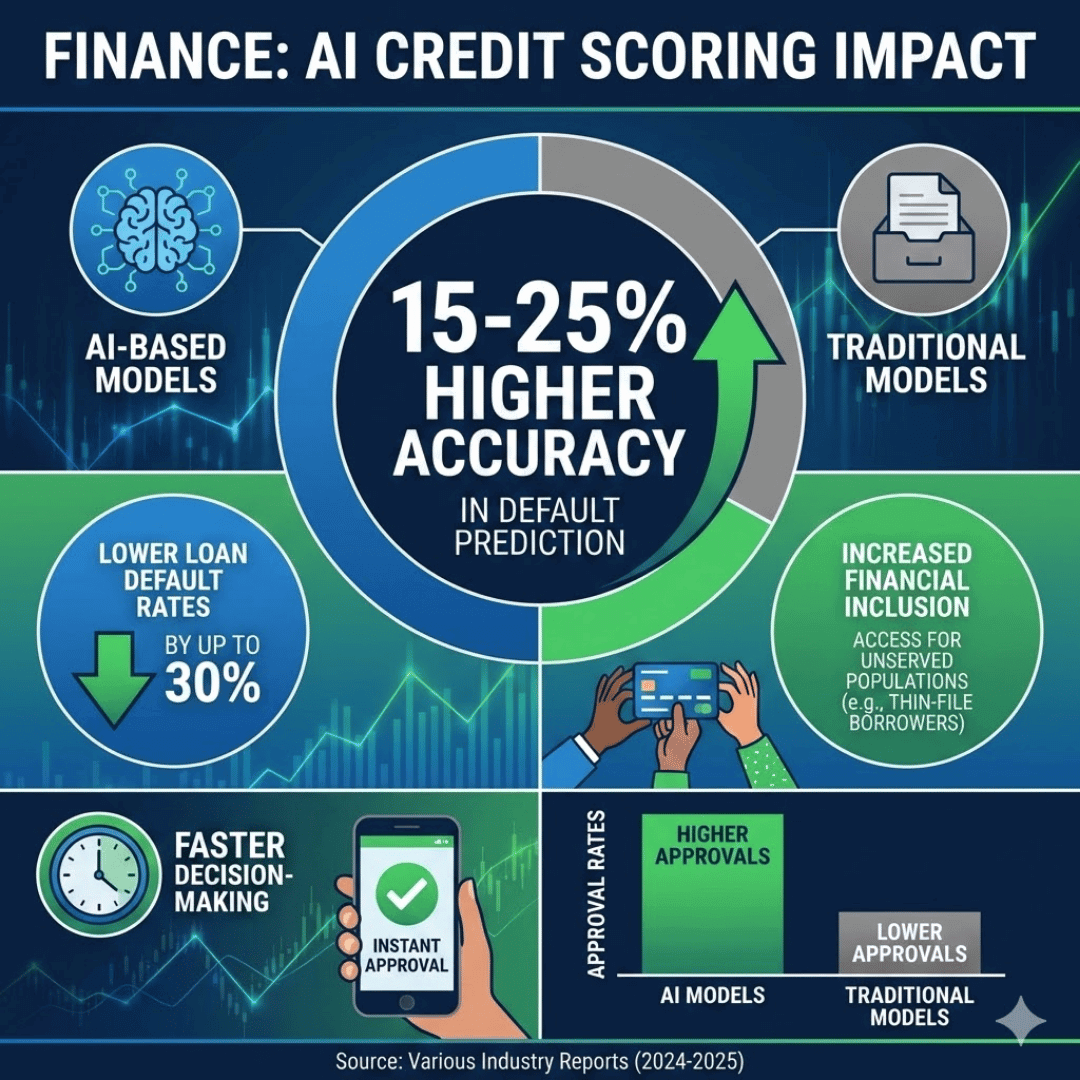

AI credit scoring changes this equation fundamentally. According to FDIC research, AI and big data adoption reduces loan default rates by 29.6% while decreasing unclassified credit ratings by 40.1%. These systems see what traditional models miss.

The adoption curve has accelerated dramatically. Research indicates that 85% of banks globally now use AI to automate lending processes. Many leverage alternative data sources to reach previously underserved populations. The transformation of credit assessment is well underway.

This guide explains how AI credit scoring works in practical terms. You will learn how these systems differ from traditional approaches. You will understand the benefits for both lenders and borrowers. You will discover the risks requiring careful management and see real examples from leading institutions.

What Is AI Credit Scoring?

AI credit scoring uses machine learning algorithms to assess borrower creditworthiness. These systems analyze vast amounts of data to predict the likelihood of loan repayment. They consider far more information than traditional credit scores.

Traditional FICO scores rely on five primary factors. Payment history, amounts owed, length of credit history, credit mix, and new credit inquiries determine scores. This narrow focus misses important signals about financial capability.

AI systems incorporate hundreds or thousands of variables. They analyze patterns in data that human analysts could never process manually. They discover relationships between variables that improve prediction accuracy significantly.

The technology does not replace human judgment entirely in most implementations. It augments decision-making by providing more accurate risk assessments. Loan officers receive better information to inform their decisions.

How Does AI Credit Scoring Work?

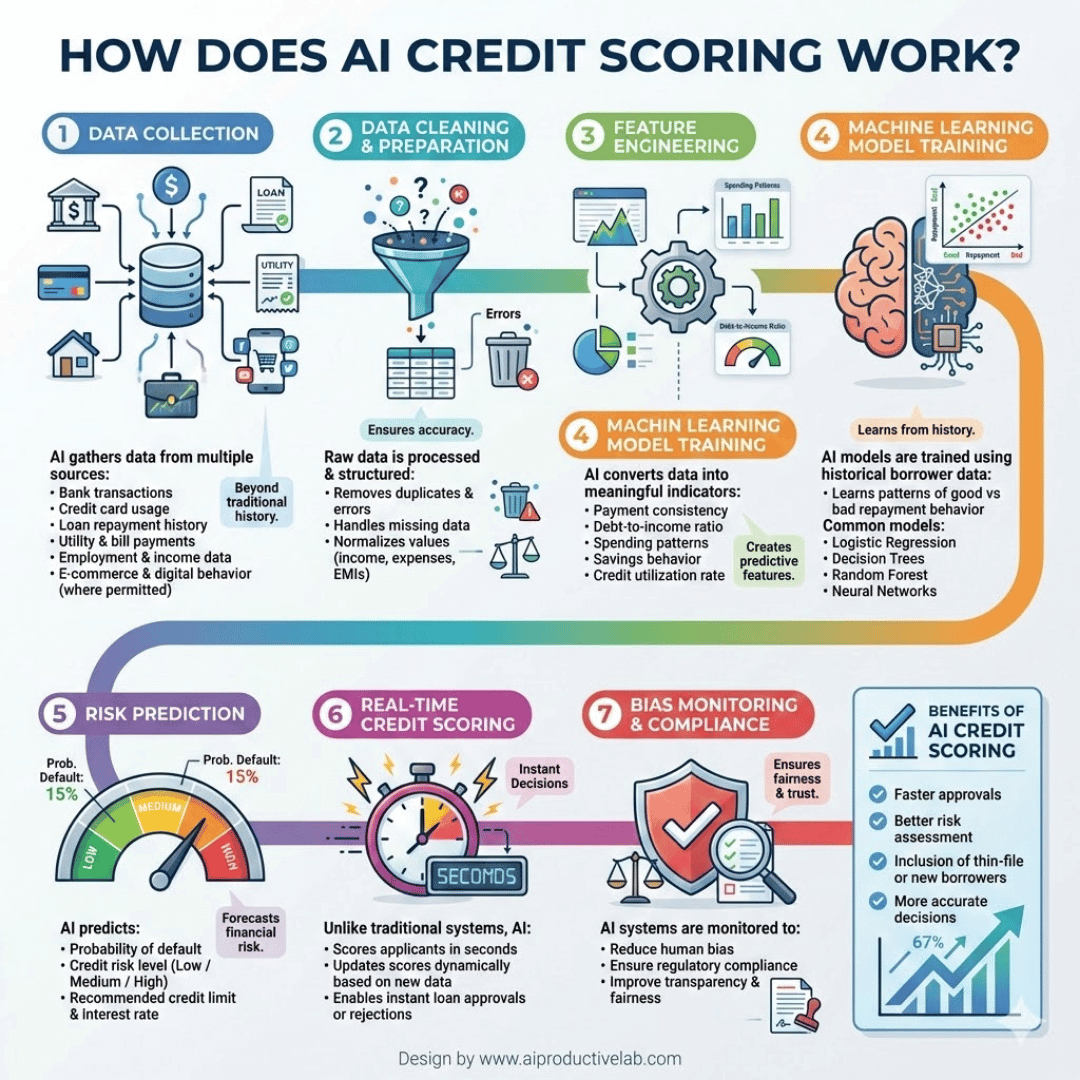

Data Collection and Alternative Data Sources

AI credit scoring begins with comprehensive data gathering. Systems collect traditional credit bureau information alongside alternative data sources.

Alternative data expands the picture of borrower creditworthiness:

- Bank account data: Cash flow patterns, balance trends, and transaction history

- Payment records: Rent, utilities, phone bills, and subscription payments

- Employment information: Job stability, income verification, and career trajectory

- Educational background: Degrees, institutions, and completion status

- Digital footprint: Online behavior patterns and device information

This broader data set enables assessment of borrowers with thin credit files. People new to credit or recovering from past difficulties get fairer evaluation. The system sees current financial behavior, not just historical credit accounts.

Machine Learning Model Training

AI systems learn from historical loan performance data. They analyze thousands of past loans to identify patterns predicting repayment or default. Supervised learning algorithms discover which variables matter most.

Training requires careful attention to data quality and representation. Biased training data produces biased models. Data scientists must ensure training sets reflect intended lending populations fairly.

Common machine learning approaches include gradient boosting, neural networks, and ensemble methods. Each offers different tradeoffs between accuracy and interpretability. Model selection depends on regulatory requirements and business needs.

Risk Prediction and Scoring

Trained models evaluate new loan applications by analyzing applicant data against learned patterns. They calculate probability of default and assign risk scores. Higher scores indicate lower risk borrowers.

AI scores often prove more predictive than traditional credit scores. They capture nuances that simple scoring formulas miss. Better predictions mean fewer defaults and more approved loans.

Some systems provide continuous scores rather than single numbers. They show confidence intervals and identify factors driving assessments. This additional context helps loan officers make informed decisions.

Continuous Learning and Model Updates

Credit markets evolve constantly. Economic conditions change borrower behavior. New fraud schemes emerge. AI systems must adapt to maintain accuracy.

Continuous learning incorporates new loan outcomes into model training. Systems observe which predictions proved accurate and adjust accordingly. Performance improves over time as models accumulate experience.

Regular model validation ensures ongoing accuracy and fairness. Lenders monitor for drift in model performance. They retrain or adjust models when accuracy degrades.

Benefits of AI Credit Scoring

For Lenders

AI credit scoring delivers substantial advantages to lending institutions:

- Improved accuracy: AI models predict default more accurately than traditional scores, reducing losses

- Faster decisions: Automated analysis enables instant or near-instant lending decisions

- Reduced costs: Automation decreases manual underwriting expenses significantly

- Expanded market: Better risk assessment enables lending to previously declined segments

- Consistent evaluation: AI applies criteria uniformly without human inconsistency

- Fraud detection: Pattern recognition identifies suspicious applications automatically

- Portfolio optimization: Better risk understanding improves overall portfolio performance

For Borrowers

Borrowers benefit significantly from AI credit assessment:

- Fairer evaluation: AI considers current financial behavior, not just historical credit

- Faster approval: Instant decisions eliminate waiting for manual review

- Expanded access: Alternative data enables approval for thin-file borrowers

- Better pricing: Accurate risk assessment means appropriate rates for each borrower

- Second chances: Recent positive behavior can overcome past credit difficulties

- Financial inclusion: Previously excluded populations gain access to formal credit

Risks and Challenges of AI Credit Scoring

Algorithmic Bias Concerns

AI systems can perpetuate or amplify existing biases. Models trained on historically biased lending data may discriminate against protected groups. Even neutral-seeming variables can serve as proxies for prohibited factors.

Fair lending laws require equal treatment regardless of race, gender, or other protected characteristics. AI systems must comply with these requirements. Regular testing for disparate impact is essential.

Addressing bias requires intentional effort throughout model development. Diverse teams catch problems homogeneous groups might miss. Fairness constraints can be built into model training. Ongoing monitoring detects emerging bias issues.

Explainability Requirements

Regulations require lenders to explain adverse actions to declined applicants. Complex AI models may not provide clear explanations. The “black box” nature of some algorithms creates compliance challenges.

Explainable AI techniques help address transparency requirements. They identify factors most influencing individual decisions. Simpler models sacrifice some accuracy for interpretability.

Lenders must balance predictive power against explainability needs. Regulatory guidance continues evolving on acceptable approaches. Staying current with requirements demands ongoing attention.

Data Privacy and Security

AI credit scoring requires extensive personal data. Collection, storage, and use raise privacy concerns. Consumers may not understand how their information influences lending decisions.

Data security becomes critical with sensitive financial information. Breaches could expose applicants to identity theft or other harms. Robust security practices protect both consumers and lenders.

Privacy regulations like GDPR and CCPA impose requirements on data handling. Consent, transparency, and data minimization principles apply. Compliance adds complexity to AI implementation.

Model Risk Management

AI models can fail in unexpected ways. They may perform poorly when economic conditions differ from training data. Adversarial manipulation could exploit model vulnerabilities.

Effective model risk management requires robust validation and monitoring. Lenders must test models thoroughly before deployment. Ongoing performance tracking detects problems early.

Regulatory scrutiny of AI model risk has increased significantly. Examiners evaluate model governance, validation, and oversight. Strong risk management practices satisfy regulatory expectations.

Real-World Examples of AI Credit Scoring

Upstart: AI-Native Lending

Upstart built their lending platform on AI credit scoring from the beginning. Their models consider over 1,600 variables including education and employment alongside traditional credit data.

The company reports significantly lower default rates compared to traditional scoring at similar approval rates. Their approach enables lending to borrowers traditional models would decline. Upstart demonstrates what purpose-built AI credit assessment can achieve.

ZestFinance: Machine Learning Credit Models

ZestFinance develops AI credit scoring technology for lenders. Their ZAML platform enables financial institutions to build and deploy machine learning models. The technology emphasizes both accuracy and explainability.

The company works with major banks, credit unions, and fintech lenders. Clients report improved approval rates with maintained or reduced default rates. ZestFinance shows how AI credit scoring scales across different lending contexts.

Kabbage (American Express): Small Business Lending

Kabbage revolutionized small business lending using AI credit assessment. Their systems analyze business bank accounts, accounting software, and payment processing data. Real-time data provides current pictures of business health.

Traditional small business lending required extensive documentation and manual review. Kabbage approves loans in minutes based on AI analysis. American Express acquired the company to enhance their small business offerings.

LenddoEFL: Financial Inclusion

LenddoEFL focuses on credit scoring for emerging markets where traditional credit data is scarce. Their AI analyzes alternative data including psychometric assessments and digital behavior patterns.

The company serves lenders across Asia, Africa, and Latin America. Their approach enables lending to populations with no formal credit history. LenddoEFL demonstrates AI enabling financial inclusion globally.

JPMorgan Chase: Enterprise AI Credit Assessment

JPMorgan Chase applies AI across their massive lending operations. Machine learning models enhance credit decisions for consumer and commercial lending. The bank continues expanding AI applications in credit assessment.

Their scale enables AI training on enormous datasets. Sophisticated models improve accuracy across diverse lending products. JPMorgan illustrates how traditional banks adopt AI credit capabilities.

How to Implement AI Credit Scoring

Step 1: Define Objectives and Requirements

Clarify what you want AI credit scoring to achieve. Common objectives include improving accuracy, expanding approval rates, reducing costs, or reaching new markets. Different goals require different approaches.

Identify regulatory requirements governing your lending. Fair lending laws, adverse action requirements, and model risk expectations shape implementation options. Legal and compliance teams must participate in planning.

Step 2: Assess Data Assets and Gaps

Evaluate available data for AI model development. Traditional credit bureau data provides foundation. Alternative data sources expand predictive power.

Identify data quality issues requiring remediation. AI systems require clean, consistent data to function effectively. Investment in data infrastructure often precedes successful AI implementation.

Step 3: Choose Build Versus Buy Approach

Decide whether to develop custom AI capabilities or purchase vendor solutions. Consider your technical resources, timeline requirements, and competitive differentiation needs.

Vendor solutions offer faster deployment and proven performance:

- Speed: Pre-built models deploy in weeks rather than months

- Expertise: Vendors bring specialized AI credit experience

- Compliance: Established solutions address regulatory requirements

- Cost: Shared development costs reduce individual burden

Custom development enables tailored approaches:

- Differentiation: Proprietary models create competitive advantage

- Control: Direct ownership of technology and data

- Flexibility: Custom solutions address unique requirements

- Integration: Purpose-built for existing systems

Most organizations adopt hybrid strategies combining vendor components with custom elements.

Step 4: Develop and Validate Models

Build or configure AI credit models using historical loan data. Ensure training data represents intended lending populations fairly. Test for accuracy and bias before deployment.

Validation must satisfy regulatory expectations. Independent review of model performance provides assurance. Documentation supports examination and audit requirements.

Step 5: Deploy With Appropriate Governance

Implement AI credit scoring with strong oversight and monitoring. Define roles and responsibilities for model governance. Establish procedures for ongoing performance tracking.

Start with limited deployment to build confidence. Expand gradually as performance proves satisfactory. Maintain fallback procedures for system failures.

Step 6: Monitor and Improve Continuously

Track model performance against expectations rigorously. Monitor for accuracy degradation, bias emergence, and changing market conditions. Regular retraining maintains effectiveness.

Incorporate feedback from lending outcomes. Confirmed defaults and successful repayments inform model improvement. Continuous learning sustains competitive advantage.

Conclusion

AI credit scoring represents a fundamental advancement in lending technology. Machine learning models predict default more accurately than traditional approaches. Alternative data enables assessment of borrowers invisible to conventional scoring. The benefits extend to both lenders and borrowers.

Implementation requires careful attention to fairness, explainability, and regulatory compliance. Bias concerns demand intentional mitigation throughout model development. Transparency requirements shape acceptable approaches. Strong governance ensures responsible deployment.

The institutions mastering AI credit scoring gain significant advantages. They approve more loans with lower default rates. They reach underserved markets profitably. They operate more efficiently than competitors relying on outdated methods.

The transformation of credit assessment is well underway. Early adopters build capabilities that compound over time. Organizations considering AI credit scoring should act thoughtfully but promptly.

Explore how AI credit scoring could transform your lending operations. Talk to our experts to understand which approaches fit your specific market, regulatory environment, and business objectives.

FAQs

AI credit scoring uses machine learning algorithms to assess borrower creditworthiness by analyzing traditional credit data alongside alternative data sources. It predicts loan repayment probability more accurately than traditional scores.

Research shows AI credit models reduce default rates by up to 29.6% compared to traditional scoring. They capture patterns and relationships that simple scoring formulas miss.

AI credit scoring may analyze bank account transactions, rent and utility payments, employment history, educational background, and digital behavior patterns alongside traditional credit bureau data.

AI credit scoring must comply with fair lending regulations prohibiting discrimination. Lenders must test for bias, provide adverse action explanations, and maintain appropriate model governance.

Implementation timelines range from weeks for vendor solutions to months for custom development. Pilots can demonstrate value quickly before broader deployment.

AI/ML Strategy and Consulting

AI/ML Strategy and Consulting Data Science And Data Analytics

Data Science And Data Analytics Generative AI

Generative AI AI Consulting Services

AI Consulting Services AI Automation Solutions

AI Automation Solutions API Integration

API Integration